Free Money Cheat Sheets

Level-Up Your Finances with Cheat Sheets Built for Busy Employees

These products are for educational purposes only and is not financial advice. Please review our terms and conditions before downloading. Consult with a financial advisor before making any financial decisions.

Download each cheat sheet using the email fields at the foot of each sheet.

These four money cheat sheets were designed to give you clear, actionable frameworks you can implement immediately. Each sheet condenses complex personal finance topics into simple visuals, tables, and step-by-step plans.

Whether you’re trying to build an emergency fund, pay off credit card debt faster, understand compound interest, or maximize tax-advantaged accounts, these guides provide the exact strategies used by people who have achieved financial freedom.

The 4 Money Cheat Sheets Included

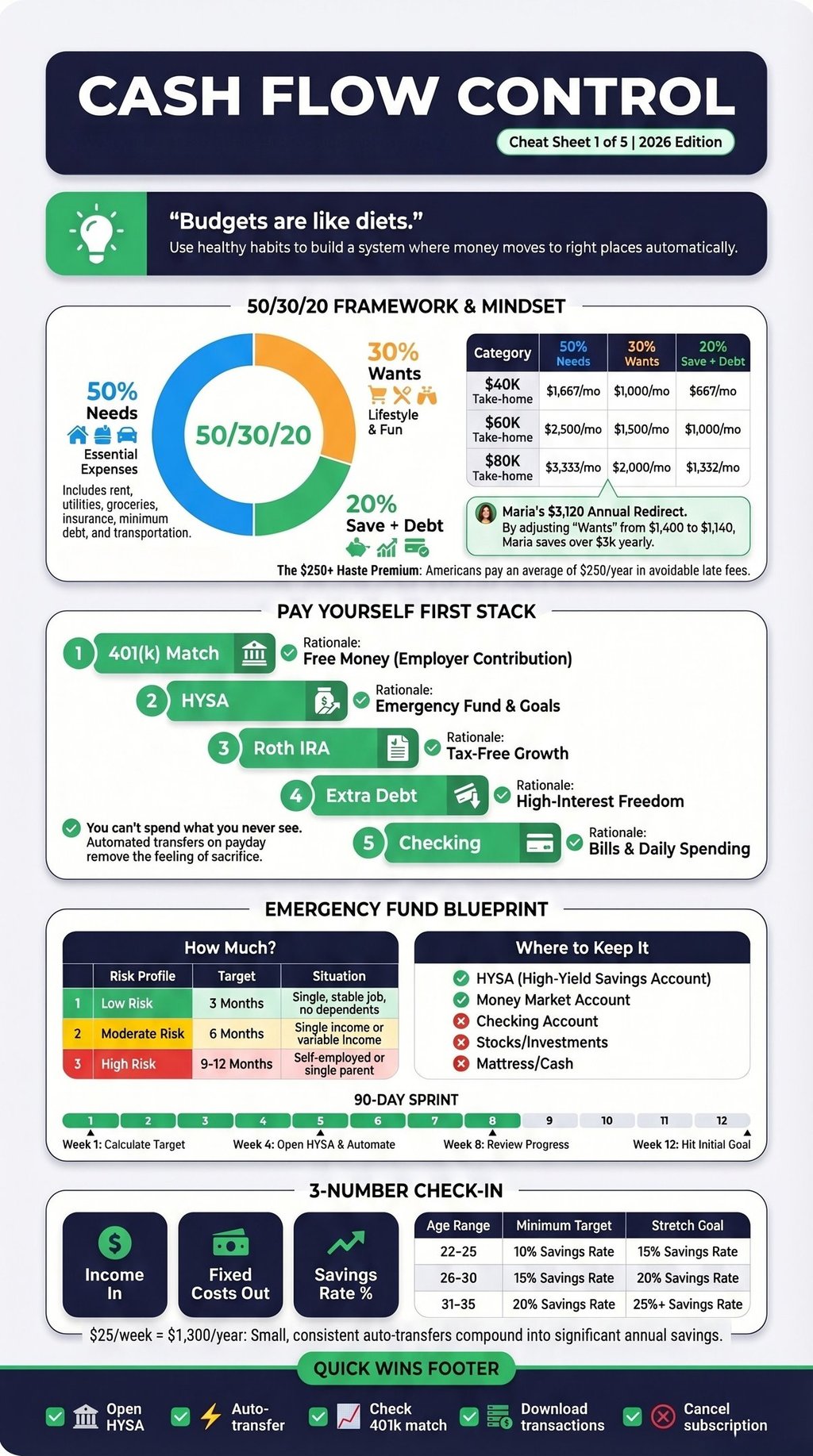

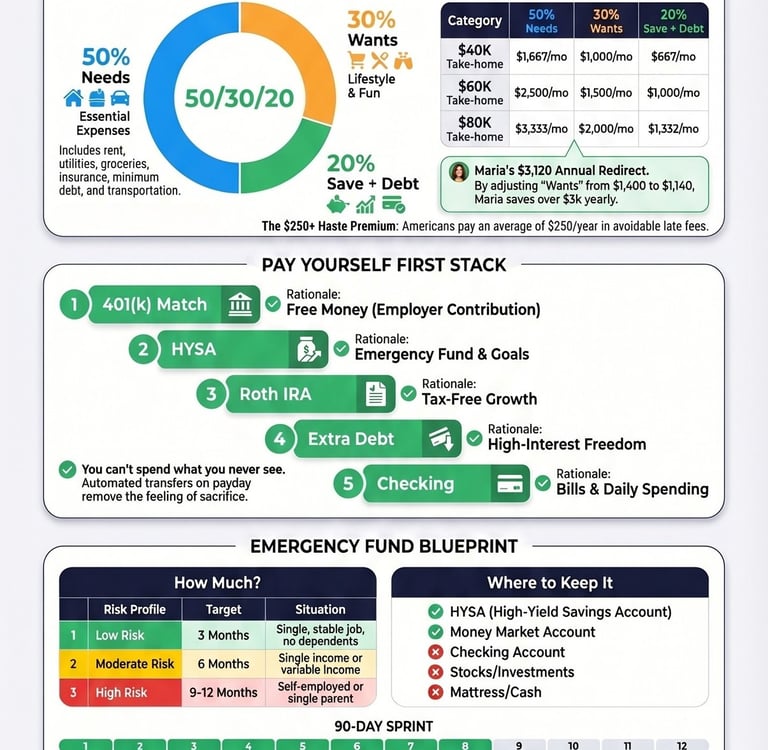

1. Cash Flow Control Cheat Sheet

Master your monthly money flow with the proven 50/30/20 framework and a “Pay Yourself First” priority stack.

Key sections include:

50/30/20 budget breakdown with real dollar examples

5-step Pay Yourself First order (401(k) match → HYSA → Roth IRA → Extra debt → Checking)

Emergency fund targets by risk level

90-day sprint timeline

3-number check-in system for ongoing progress

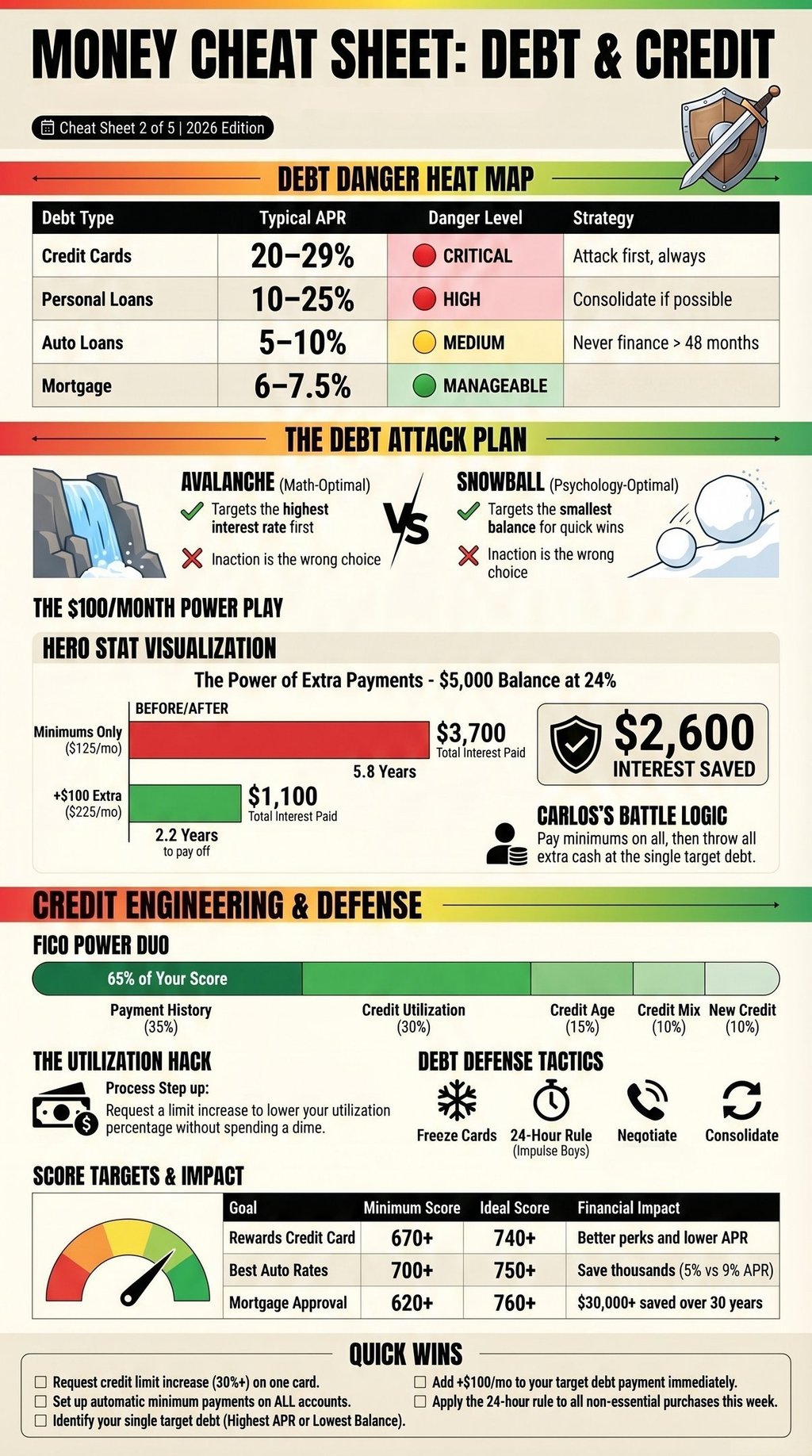

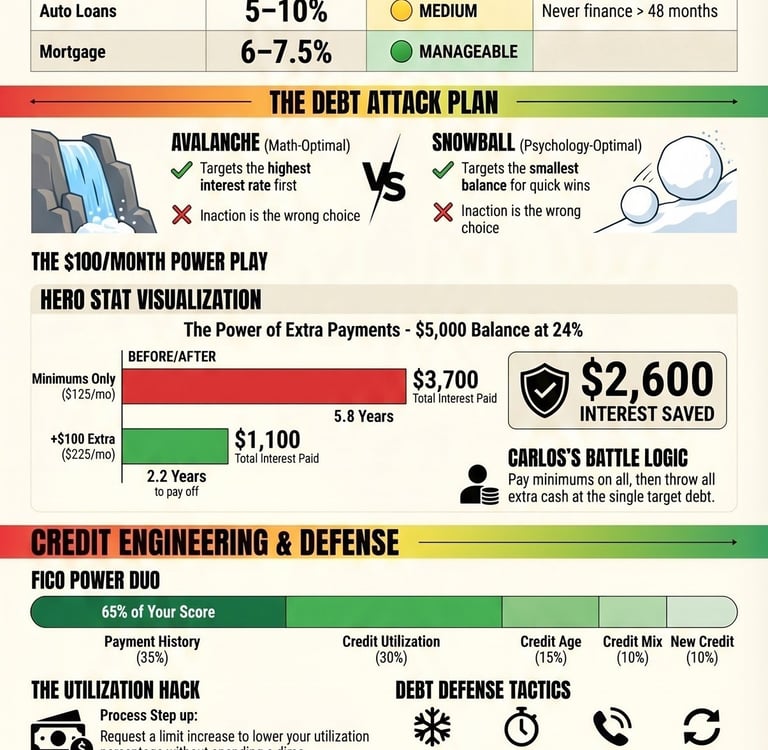

2. Debt & Credit Cheat Sheet

Learn how to attack debt strategically and protect your credit score.

Key sections include:

Debt Danger Heat Map (APR ranges and danger levels)

Debt Avalanche vs. Snowball comparison

The $100/month power play example

FICO score breakdown and utilization hack

Credit defense tactics and score targets for rewards, auto loans, and mortgages

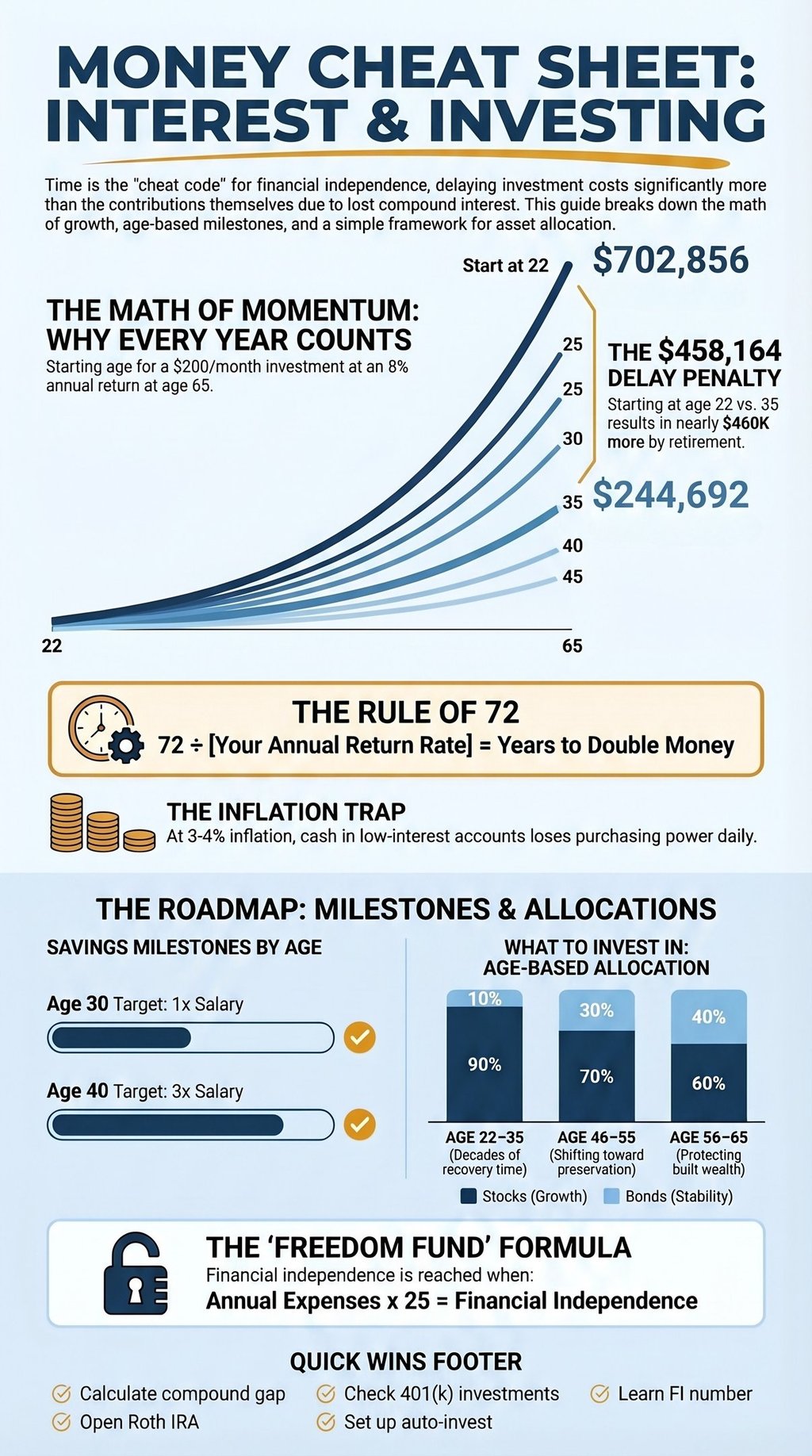

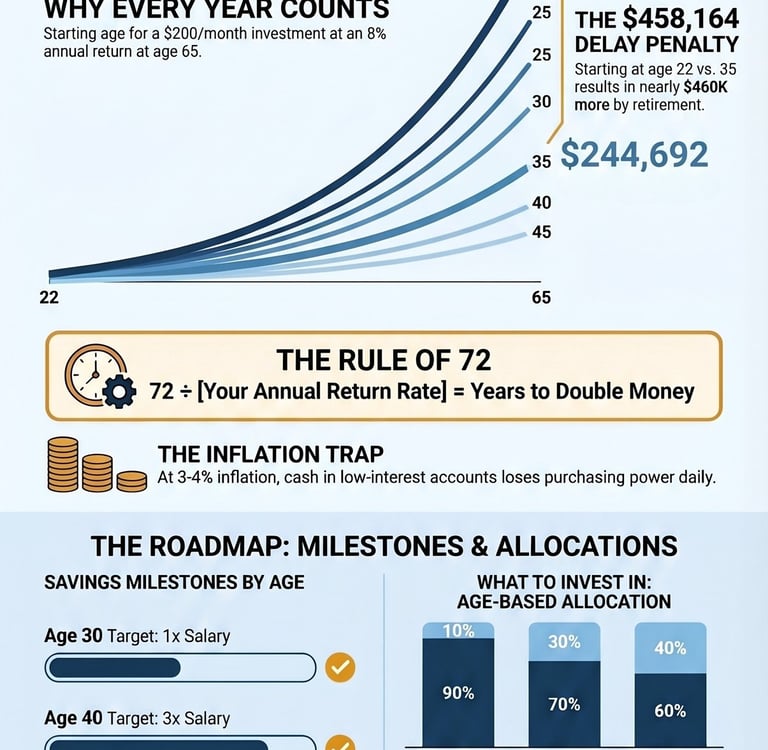

3. Interest & Investing Cheat Sheet

Understand the true power of time and compound growth.

Key sections include:

The Math of Momentum (starting at age 22 vs. 35)

Rule of 72 explained

Inflation trap warning

Savings milestones by age (1× salary at 30, 3× at 40)

Age-based asset allocation

Freedom Fund Formula (25× annual expenses)

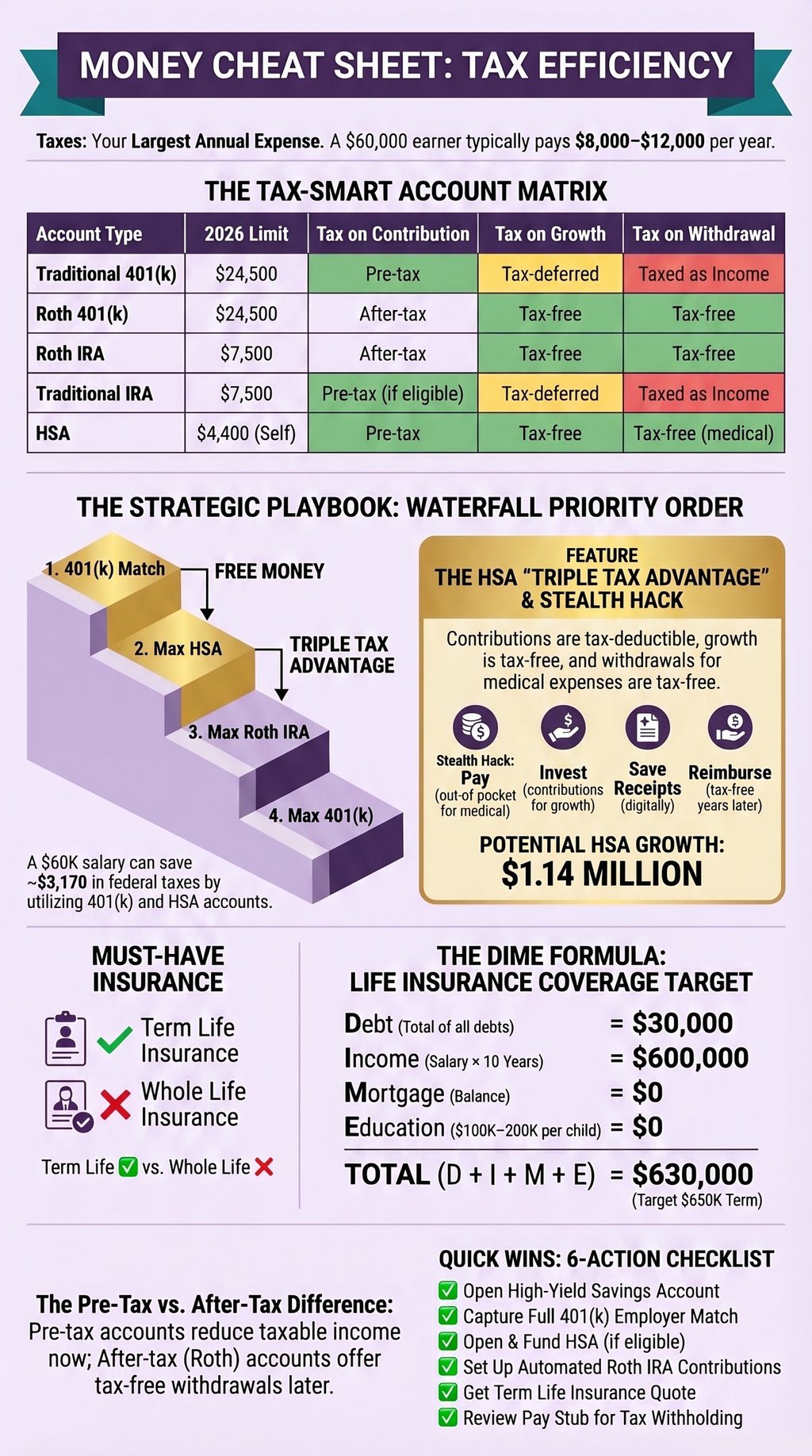

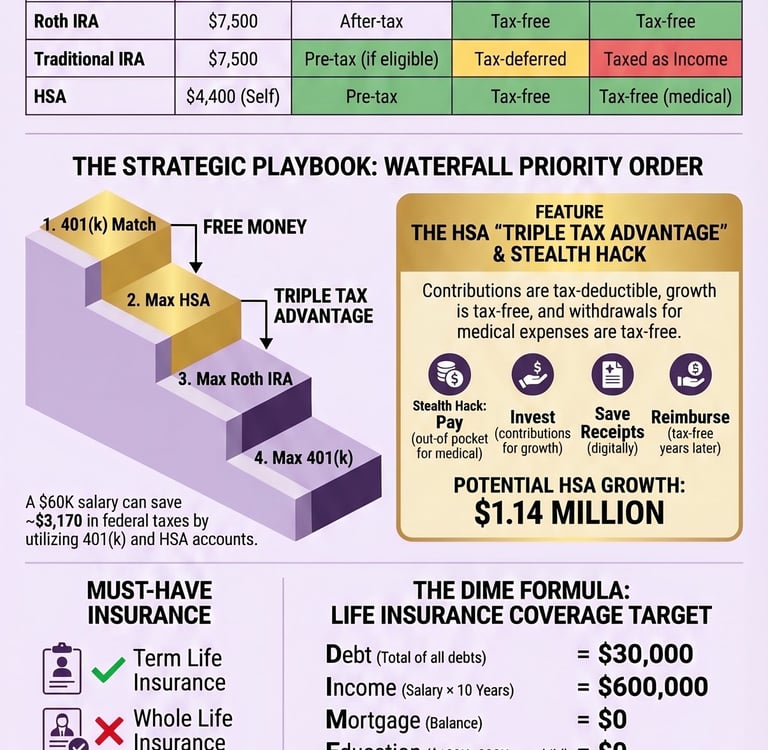

4. Tax Efficiency Cheat Sheet

Minimize your largest annual expense with smart account choices.

Key sections include:

Tax-Smart Account Matrix (Traditional 401(k), Roth 401(k), Roth IRA, HSA)

Strategic Waterfall Priority Order

HSA Triple Tax Advantage and stealth hack

Term life vs. whole life insurance comparison

DIME Formula for life insurance coverage

6-action quick wins checklist

Why These Cheat Sheets Work

Visual and scannable — perfect for quick reference

Based on proven financial principles (50/30/20, debt avalanche, Rule of 72, HSA triple tax advantage)

Include specific dollar examples and targets

Designed for 2026 tax limits and current economic conditions

Printable and mobile-friendly

How to Get Your Free Cheat Sheets

Enter your email below each cheat sheet to receive instant access. You’ll also join our newsletter for weekly money tips, new frameworks, and updates.

FAQ

What is the 50/30/20 budget rule?

The 50/30/20 rule allocates 50% of income to needs, 30% to wants, and 20% to savings and debt repayment.

Should I use the debt avalanche or debt snowball method?

The avalanche method saves the most money by targeting highest-interest debt first. The snowball method provides psychological wins by paying smallest balances first.

What is the Rule of 72?

Divide 72 by your expected annual return rate to estimate how many years it takes for your money to double.

What is the Freedom Fund Formula?

Multiply your annual expenses by 25 to calculate the amount needed for financial independence.

Why is an HSA so powerful?

An HSA offers triple tax advantages: tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses.

How much should I have in an emergency fund?

Most people should aim for 3–6 months of expenses. Higher-risk situations may require 9–12 months.

What is the best order for retirement accounts?

Capture your full 401(k) employer match first, then max an HSA (if eligible), then max a Roth IRA, then max the rest of your 401(k).

CheatCode Wealth™

Build your wealth. Keep your life.

© 2025. All rights reserved. Cheatcode Wealth LLC. This webpage may contain paid affiliate links.