What is Stairstep Retirement? The Complete Guide to Frontloading Freedom

Stairstep Retirement is a flexible wealth-building strategy that lets you work less when life demands it most and ramp up later. Learn the complete framework from its creator, Garrett Duyck.

RETIREMENTWORK-LIFE BALANCE

Garrett Duyck

6/30/20269 min read

If you've spent any time in the personal finance world, you've probably noticed a pattern: every retirement strategy seems to demand that you sacrifice your best years now so you can enjoy life later.

Work 60-hour weeks in your 30s. Max out every account. Skip vacations. Then, if everything goes perfectly, you might get to relax at 65. Or maybe 45, if you're willing to eat rice and beans for a decade.

I want to share a different approach: one my wife and I have been living for years. We call it Stairstep Retirement, and it starts with a question most financial advice never asks:

What if you could design your life so that you have more time right now, during the years that matter most?

What Stairstep Retirement Actually Is

Stairstep Retirement is a flexible wealth-building strategy where you intentionally adjust your work intensity up and down across different life stages, rather than grinding at full speed until some distant finish line.

The core idea is simple: frontload freedom, backload work. Adjust accordingly.

Instead of working maximum hours during your 20s, 30s, and 40s while your kids are growing up, your health is strong, and your energy is high, you strategically reduce your work hours during the seasons of life when time is most valuable. Then, when your life circumstances change (kids are older, more bandwidth becomes available), you ramp back up to accelerate wealth-building.

Think of it like a staircase. You step down when life calls for it. You step back up when you're ready.

What Stairstep Retirement Is NOT

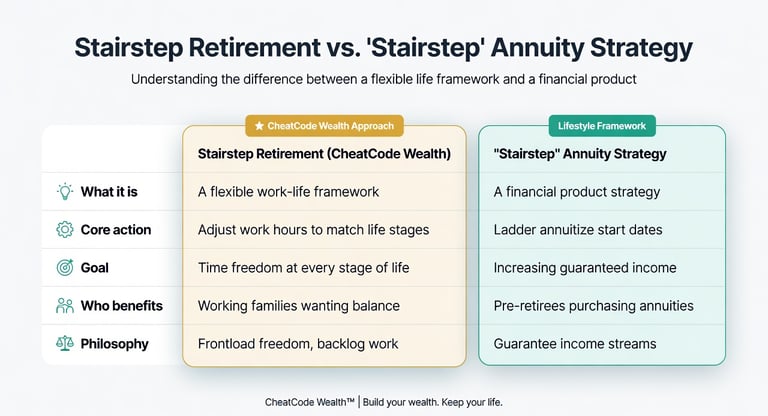

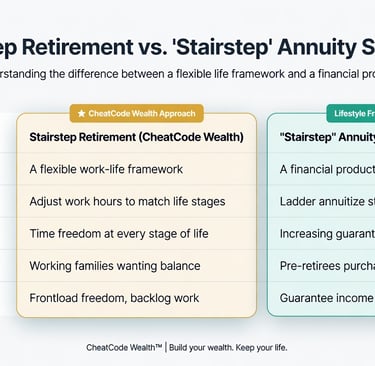

Before we go further, let me clear up some confusion. If you search "stairstep retirement" online, you might find some financial advisors using the phrase to describe an annuity laddering strategy, where you stagger the start dates of multiple income annuities to create increasing cash flow.

That is not what we're talking about here.

Stairstep Retirement, as I define it, is a lifestyle design philosophy, not a financial product. It's about how you structure your relationship with work across your entire career, not how you structure annuity payments. No one is trying to sell you an insurance product.

Now that we've cleared that up, let's dig into how it actually works.

The Origin Story: Why I Created Stairstep Retirement

My wife and I did what most people do: we optimized for stability. Good jobs, good benefits, steady paychecks. But when our fourth child was born, we had four kids under ten, and I found myself asking a question that wouldn't leave me alone:

If we're already out of high-interest debt and investing, do we really need to work this many hours right now?

The math said we were doing fine. Our active income covered our expenses with a surplus. Our portfolio was on track. But the traditional advice kept telling us to push harder, save more, grind now.

The problem was, "now" was the only time our kids would be little. Every Saturday I spent working was a Saturday I didn't spend at a soccer game. Every late evening was a bedtime story I missed.

So we made a choice. I restructured my job to work around 32 hours per week. My wife took a part-time position. We intentionally stepped down on the income staircase to step up on the life staircase.

And here's the part that surprises people: we plan to step back up. When our kids are in high school and don't want to hang out with us anyway, we'll have the bandwidth to ramp up our careers and accelerate our wealth-building. That's the "stairstep." It's not a one-way exit. It's adaptive.

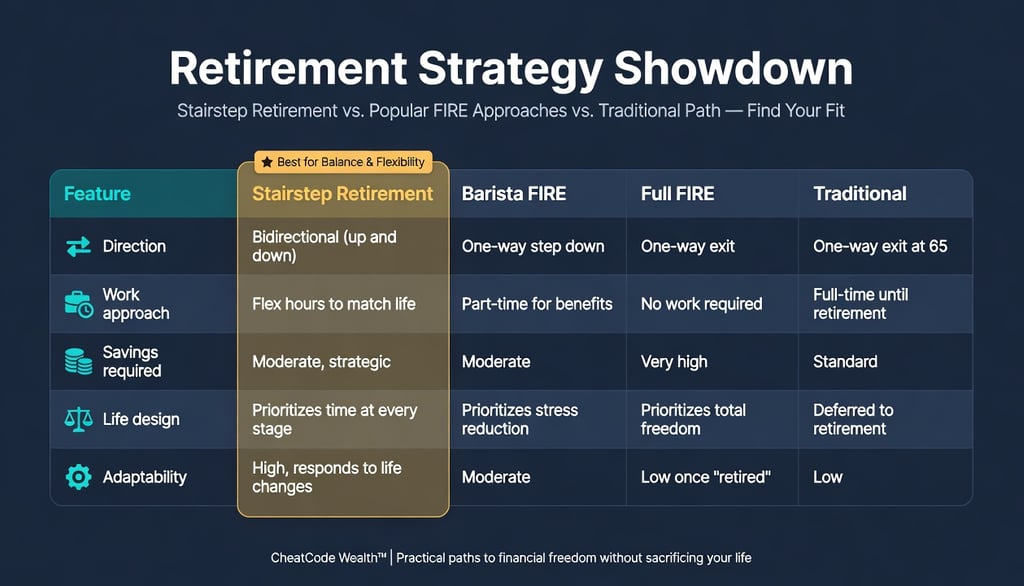

How Stairstep Retirement Differs from Traditional Retirement and FIRE

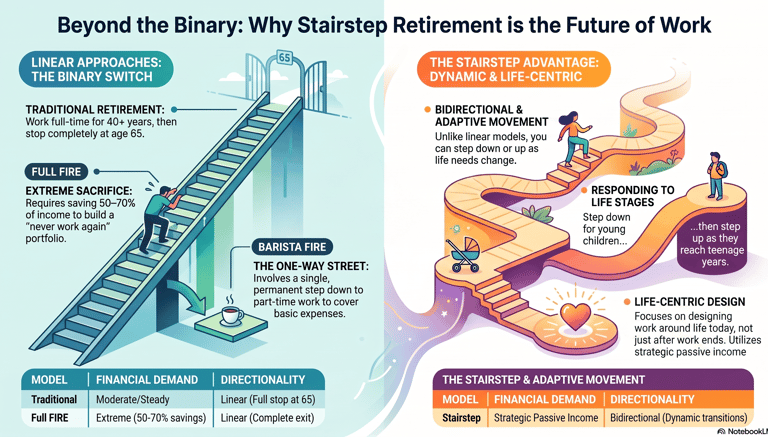

Most retirement frameworks treat your career as a straight line. You're either "on" (working full time) or "off" (retired). Even the FIRE movement, for all its innovation, often treats early retirement as a binary switch: save aggressively, then stop working entirely.

Stairstep Retirement is fundamentally different because it's adaptive and bidirectional.

vs. Traditional Retirement

Traditional retirement says: work full-time for 40+ years, then stop completely at 65. The assumption is that life happens after work ends. Yuck.

Stairstep Retirement says: life is happening right now. Design your work around your life, not the other way around.

vs. Full FIRE

The full FIRE (Financial Independence, Retire Early) approach requires aggressive saving, often 50-70% of income, to build a portfolio large enough to never work again. It's powerful, but it demands extreme frugality and often years of intense sacrifice. FIRE is not compatible with raising a family. Some people can manage it, but it's not suitable for most. It denies your children as they grow: your time, your attention, and your wallet.

Stairstep Retirement doesn't require you to save 70% of your income. It requires you to be strategic about when and how much you work, and to build passive income streams that give you flexibility.

vs. Barista FIRE

Barista FIRE is the closest cousin to Stairstep Retirement. In Barista FIRE, you accumulate enough investments to cover most of your expenses, then take a part-time job (often for health insurance) to bridge the gap.

But here's the key difference: Barista FIRE is linear. Stairstep Retirement is dynamic.

Barista FIRE assumes you step down once and stay there: leave corporate life, work part-time at Starbucks, coast to traditional retirement age. It's a one-directional transition. It can be difficult to move back into a high-paying career once you've been removed from it over time.

Stairstep Retirement plans for multiple transitions. You might step down in your 30s when your kids are young, step back up in your late 40s when they're teenagers, then step down again in your 50s as you approach true retirement. It responds to life stages, not just financial milestones.

The Three Pillars of Stairstep Retirement

Stairstep Retirement works because of three core principles:

Pillar 1: Your Job is a Wealth-Building Tool, Not a Prison

This is where we part ways with a lot of the financial independence community. You don't need to "escape" your job. You need to use it strategically.

Your employment provides a paycheck (active income), benefits (especially health insurance), and structure. The goal isn't to run away from it. The goal is to optimize it so that it serves your life instead of consuming it.

For our family, that meant choosing jobs with intentionally short commutes (8 minutes for me, 15 for my wife), negotiating schedules that protect family time, and saying no to roles that demanded evenings and weekends.

Pillar 2: Convert Paychecks into Passive Income (The Paycheck-to-Passive Method)

While you're working, a portion of your active income should be systematically converted into income-producing assets: stocks, bonds, real estate, options, digital products, or any of the seven classes of income-producing assets.

Over the past decade, my wife and I have built over $50,000 in annual passive income through disciplined investing. We currently reinvest all of it, but that income stream is what gives us the confidence to work fewer hours without financial anxiety. When we eventually step down further, those assets will replace an increasing share of our active income.

One of the main criticisms of Stairstep retirement is that it does not fully take advantage of the power of compounding. This is true; it does not maximize investments at a young age to compound over decades and reach exponential growth. This is an acceptable trade-off for the ability to enjoy and experience more of life in our youth.

When you and your children are young, these are the real golden years. Ask any grandparents, and they will tell you the same thing. A wise stair-step retirement strategy does not ignore the power of compounding; we still invest, and our investments are reinvested. But we also recognize the potential returns on investment of the time that we spend with our children throughout their lives. That is difficult to quantify but worth every bit of compound interest forgone.

Pillar 3: Time is the Real Currency

This is the philosophical heart of Stairstep Retirement. Most financial advice optimizes for dollars. We optimize for time.

When my wife was offered a $50,000 retention bonus to stay in a position that required weekends, she turned it down. On paper, that looks irrational. In real life, it bought back every weekend with our family. That's a trade we'd make again in a heartbeat.

You can sit down and try to pencil out what $50,000 would be worth, invested and grown over 30 years. Don't! It doesn't matter. First, I'm not interested in selling my time for that financial gain. Second, people consistently underestimate the opportunity cost of postponing the life they want. I have had many dear friends and family who have passed away at a young age and never enjoyed the fruits of their careful, disciplined labor.

The question we always ask is: At this point in our lives, is the value of additional income greater than the value of additional time? When the answer is no, we step down. When the answer shifts, we step back up.

The MAP System: The Engine Behind Stairstep Retirement

Stairstep Retirement isn't just a philosophy. It's powered by a practical framework I call the MAP System:

M — Master Your Money: Get control of your spending. Eliminate high-interest debt. Build an emergency fund. Understand where every dollar goes. This is the foundation: you can't step down from work if you don't have control over your spending.

A — Accelerate Your Earnings: Optimize your active income. This doesn't mean working more hours. It means earning more per hour. Negotiate raises, develop high-value skills, choose roles with better compensation-to-time ratios.

P — Perpetuate Your Income: Convert active income into passive income streams. Build or buy assets that generate income whether you're working or not. This is the Paycheck-to-Passive transition that makes stepping down financially possible.

When you've progressed through all three levels, you've built the financial engine that gives you the freedom to adjust your work intensity without financial stress.

Who is Stairstep Retirement For?

Stairstep Retirement isn't for everyone, and I want to be honest about that. It works best for people who:

Value time with family during specific life stages (young children, aging parents, personal health needs)

Want to keep working but on their own terms, not someone else's

Are willing to earn less now in exchange for more presence and flexibility

Plan to ramp back up later when life circumstances change

Have reached basic financial stability: debt-free (except maybe a mortgage), positive net worth, active income covering expenses with a surplus, portfolio on track

It's probably NOT for you if:

You want to stop working entirely as soon as possible (look at Full FIRE)

You're in a financial crisis and need to maximize income immediately

You're unwilling to accept a lower income during step-down periods

Getting Started: Your First Steps

If Stairstep Retirement resonates with you, here's how to begin:

Know your numbers. What are your monthly expenses? What's your current savings rate? What does your investment portfolio look like? You can't design a step-down if you don't know your financial baseline.

Calculate your "enough for now" number. This is the minimum income needed to cover your expenses, maintain your savings goals, and stay above your financial waterline. It's not your forever number. It's your "right now" number.

Identify your time priorities. What would you do with an extra 10 hours per week? If the answer lights you up, that's your motivation.

Explore flexibility in your current role. Can you negotiate a compressed schedule? Reduce travel? Shift to part-time? Many employers are more flexible than you think, especially if you're a strong performer. Here are seven ways to get more time off without quitting your job.

Start building passive income. Even $100/month in dividend income is a start. The Paycheck-to-Passive journey begins with the first asset.

Frequently Asked Questions

Q: Isn't stepping down from work risky?

A: It can be, which is why the MAP System matters. You don't step down until you've mastered your money and have a financial cushion. The step-down trigger occurs when the value of your surplus income falls below the value of your time, but you must stay above your expense waterline. If you need help deciding, try our freedom time calculator.

Q: What if my employer won't let me reduce hours?

A: Not every job allows flexibility, and that's one of the honest tradeoffs. One of my biggest lessons is that I wish I'd chosen a Stairstep-compatible career earlier. If your current role doesn't allow it, consider whether a lateral move to a more flexible position might be worth it.

Q: How is this different from just working part-time?

A: Working part-time is a tactic. Stairstep Retirement is a strategy. It includes the intentional plan to ramp back up, the passive income building, and the life-stage awareness that makes the step-down sustainable and temporary.

Q: Do I need to be wealthy to do this?

A: No. You need to be financially stable: debt-free except your mortgage, positive net worth, expenses covered by active income with a surplus, and a portfolio that's on track. You don't need to be rich. You need to be intentional.

Q: What about healthcare?

A: This is a real consideration. For our family, my federal employee health insurance covers our entire family of six at the same cost regardless of family size. If your step-down plan involves leaving an employer with good benefits, you'll need a healthcare strategy. This might mean keeping one spouse employed for benefits, using ACA marketplace plans, or choosing Barista FIRE-style work specifically for insurance.

Get the most out of life.

Join the Portfolios & Bedtime Stories newsletter to learn how to implement Stairstep Retirement in your own life.

CheatCode Wealth™

Build your wealth. Keep your life.

© 2025. All rights reserved. Cheatcode Wealth LLC. This webpage may contain paid affiliate links.